You work hard to build your superannuation. So it's important to know who gets your super if you die.

Your super is an income source in retirement, there to help fund the life you and your family want to live when you stop working.

You need to tell your super fund who should receive your super and any life insurance when you die. Without it, your fund may decide who gets your money - and that might not match what you would’ve wanted or could delay it being paid to the people you want it to go to.

Having a valid binding beneficiary makes it easier and faster for your loved ones to receive your super when you die.

What is a beneficiary nomination?

To choose who will receive your super (and any life insurance), you must nominate a beneficiary. There are different types of nominations available, allowing you to choose one or more beneficiaries.

The four types of nominations are:

- lapsing nominations (binding): The super fund, in the event of your death, must pay your super benefit to your nominated beneficiary, unless it would be unlawful to do so. This expires after a maximum period of 3 years.

- reversionary nominations (binding): The person who will receive the balance of your superannuation income stream after you die. This could be your spouse, child or other dependant.

- non-lapsing nominations (binding): A nomination that is binding with the consent of the super fund under the terms of the trust deed and does not expire after a period of time.

- non-binding nominations: Guides your super fund trustee on who should get your super if you die. The trustee is not bound to follow these instructions.

The importance of a binding nomination

Having a binding nomination will help your beneficiaries receive your super faster after your death, than having a non-binding nomination or no nomination at all.

Without a binding nomination, your super fund will decide who receives your money based on what is fair in the circumstances. If there are many people who may be eligible for your super (e.g. in blended families), this process can take a long time.

While non-binding nominations are often easier to make, they only provide guidance to the super fund about your wishes and the fund does not have follow them. This means they may make a different decision from what you want.

Who can be a beneficiary?

The person who receives your super after you pass away is often called a beneficiary. Many super funds allow members to choose their beneficiary, but there are rules about who is eligible. People super funds are allowed to pay your super to include:

- your current spouse or partner

- your children (of any age)

- someone who is in an interdependent relationship with you

- anybody financially dependent on you when you die

- your estate or legal personal representative.

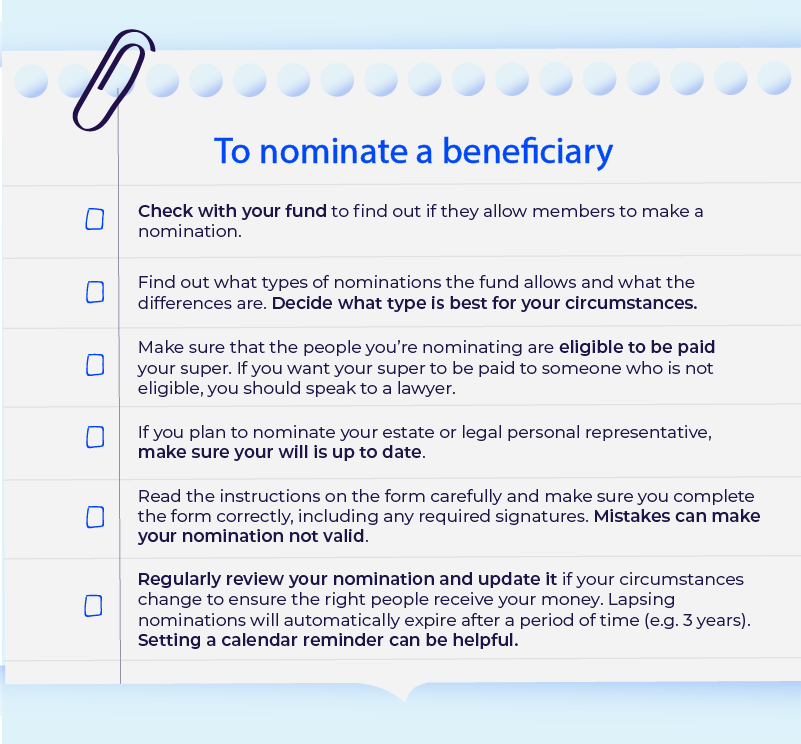

How to nominate a beneficiary

Text version: How to nominate a beneficiary

To nominate a beneficiary:

- Check with your fund to find out if they allow members to make a nomination.

- Find out what types of nominations the fund allows and what the differences are. Decide what type is best for your circumstances.

- Make sure that the people you’re nominating are eligible to be paid your super. If you want your super to be paid to someone who is not eligible, you should speak to a lawyer.

- If you plan to nominate your estate or legal personal representative, make sure your will is up to date.

- Read the instructions on the form carefully and make sure you complete the form correctly, including any required signatures. Mistakes can make your nomination not valid.

- Regularly review your nomination and update it if your circumstances change to ensure the right people receive your money. Lapsing nominations will automatically expire after a period of time (e.g. 3 years). Setting a calendar reminder can be helpful.

Adina makes a lapsing nomination

Adina is 53 years old, and lives with her husband, Sunil, and their two adult children, Mark and Margot. Adina and Sunil both work full time, and Adina has about $300,000 in super, plus $100,000 of life insurance.

After discussing it with Sunil, Adina has decided that in the case of her death, she would prefer her super and insurance to go to her husband, who can provide for their children as needed.

To ensure this, Adina visited her super fund’s website and found out that she can either make a lapsing nomination or a non-binding nomination.

- If she makes a lapsing nomination to her husband Sunil, her super fund will pay her benefit to Sunil because it’s binding.

- If she makes a non-binding nomination to Sunil, her super fund might pay Sunil or split her super between her husband and her children, Mark and Margot, because they were financially dependent on her.

Adina decides to make a lapsing nomination, reviewing the form carefully and making sure she follows all of the instructions for witnessing her signature. And, knowing that the nomination will lapse in three years, Adina puts a reminder in her calendar to review and renew her nomination a month before the expiration date.