Last updated:

Mortgage offset accounts are an important part of many households’ finances. Work out if an offset account might be right for you.

What is a mortgage offset account?

A mortgage offset account is a transaction account linked to your home loan. It’s generally available with a variable rate home loan.

The balance in the offset account reduces the amount of your loan that’s charged interest.

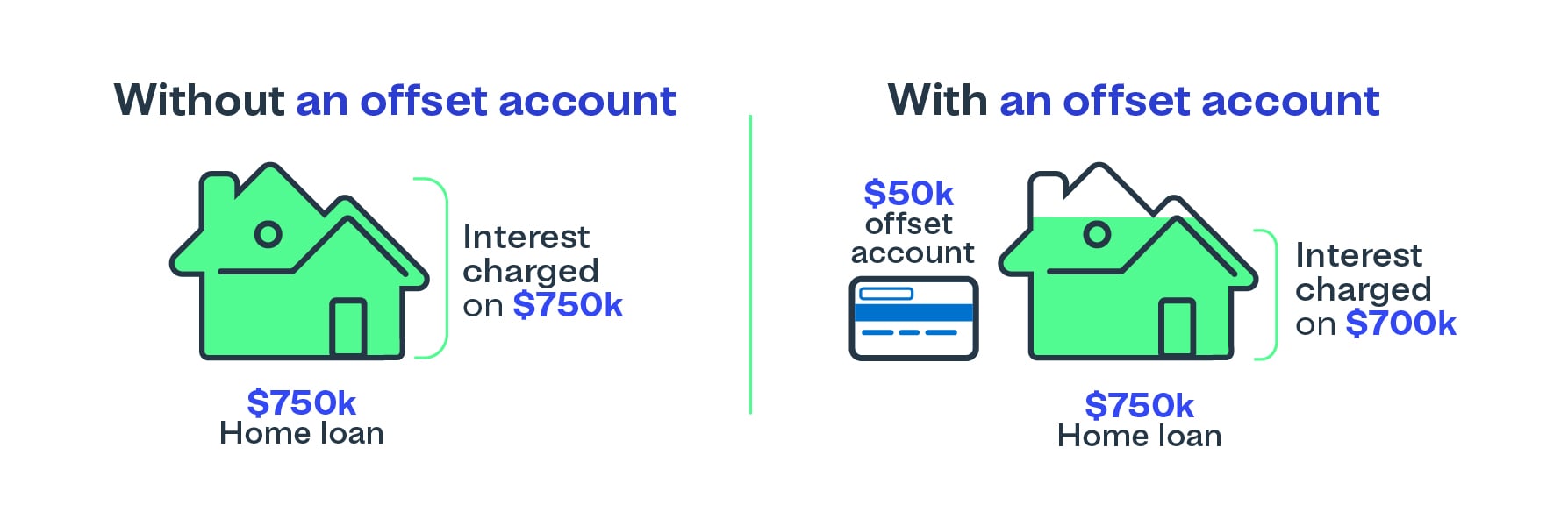

For example, if you have:

- A home loan of $750,000, and

- $50,000 in your offset account

You’ll only be charged interest on $700,000.

This means that a greater share of each loan repayment amount goes towards paying off the home loan rather than interest. Over time, this can help you pay off your mortgage sooner and reduce the total interest you pay.

How does a mortgage offset account work day-to-day?

An offset account works like an everyday bank account. You can:

- have your salary paid into it

- pay bills and set up direct debits from it

- use a debit card with it.

Interest on most home loans is calculated daily; each day, your lender subtracts your offset account balance from your loan balance before calculating interest.

The more money you keep in your offset account, and the longer it stays there, the more interest you can save.

Is it worth having an offset account?

An offset account may be worth it if you:

- have a large loan, and

- keep a regular savings balance, and

- want flexible access to your money.

It may not be worth it if:

- you usually keep a low balance in the offset account, and

- the loan has higher fees to include an offset feature, and

- the interest rate is higher than similar loans without an offset account.

Some banks charge for offset features through higher interest rates, account fees, or both. So, it’s important to compare the cost of the fees with the interest you expect to save.

The higher your loan and the larger your offset balance, the greater the potential savings. But be realistic about whether you’d be able to justify any extra cost of having an offset account.

Using a credit card with an offset account

Some people use a credit card alongside their offset account to maximise interest savings.

For example:

- have your salary paid into your offset account,

- use a credit card for everyday spending,

- pay your credit card balance in full by the due date.

This keeps more money in your offset account for longer.

However - this strategy only works if you’re sure you can repay the credit card in full each month. The average credit card interest rate, over 18% as at May 2026, is much higher than home loan interest.

The difference between an offset account and redraw facility

Both an offset account and a redraw facility can potentially help you save on interest, but they work in different ways.

An offset account: Is like a separate transaction account linked to your mortgage. You can still access your savings whenever you need them. Your savings reduce the amount of your loan that gets charged interest.

A redraw facility: These are extra payments you make that go straight onto your loan. You may be able to withdraw those extra repayments if you need to. How and when you can access them depends on your loan terms.

Before you decide whether you need either option, check your lender’s fees, interest rate, and access rules.

Warning: Check your offset account is linked properly

Millions of Australians rely on mortgage offset accounts to reduce the cost of their home loan, but an ASIC review has found customers may have been unknowingly paying more interest than they should because some banks failed to properly manage offset accounts.

If an offset account isn’t linked properly to your mortgage, the money sitting in it might not be taken into account when the bank calculates interest on your home loan. This could potentially cost you more in interest, sometimes over a long period, without you realising that something’s wrong as your loan repayments stay the same!

“When offset accounts don’t operate correctly, the harm can be hidden – loan repayments stay the same, while customers unknowingly pay more interest and take longer to repay their loan.

Customers are doubly hit – not only losing promised interest savings but also the opportunity to use that money elsewhere.”

When purchasing their home for $1 million, James and Mia borrowed $750,000 with a 30-year repayment period. They requested an offset account from their bank during loan settlement and kept an average balance of $50,000 in that account.

After one year, they noticed higher than expected interest charges and contacted their bank. The bank investigated and found it had failed to execute the offset account request, resulting in the offset not being linked for this period. With an interest rate of 6.25% per year, James and Mia inadvertently paid over $3,000 in additional interest over the year.

If the error hadn’t been detected for the life of the loan, they would have foregone nearly $230,000 of interest savings, and it would have taken them an extra four years to repay their loan.

4 actions to make sure your offset account is working for you

Follow these four key actions to get your offset account working for you.

1. Check your offset account is linked properly.

Make sure it's linked correctly through your bank’s mobile app, online banking or bank statements. Don’t assume it’s working just because you have requested one from your bank.

2. If you're unsure or can't see your interest savings, contact your bank.

Check that you’re saving money overall by having an offset account. If the savings aren’t shown in your app, online banking or statements, ask your bank.

3. Check whether your offset account needs to be relinked when your loan changes.

Refinancing or switching home loan products can break the link between your offset account and your mortgage. You may need to contact your bank to re-link it.

4. Act quickly if something looks wrong.

Offset account failures can cost you money, so contact your bank and ask questions if something doesn’t look right, is unclear or if you’re just not sure how it works.

What to consider before you apply for an offset account

Before you choose a loan with an offset account, consider:

- the interest rate – would it be lower if you didn’t select an offset eligible loan?

- any annual or package fees you’ll be charged for an offset eligible loan

- any monthly fees for the offset account

- how it compares with a redraw facility and whether a redraw facility might be more suitable.

Even small differences in interest rates and fees can add up over time, so compare your loan and features whenever your situation changes.

Learn more about choosing a home loan, and paying off your mortgage faster.

Join thousands of Australians and get tools, tips and calculators to help with your money - straight to your inbox each month.

Sign up