Last updated:

Understand your retirement income options and how they can work together.

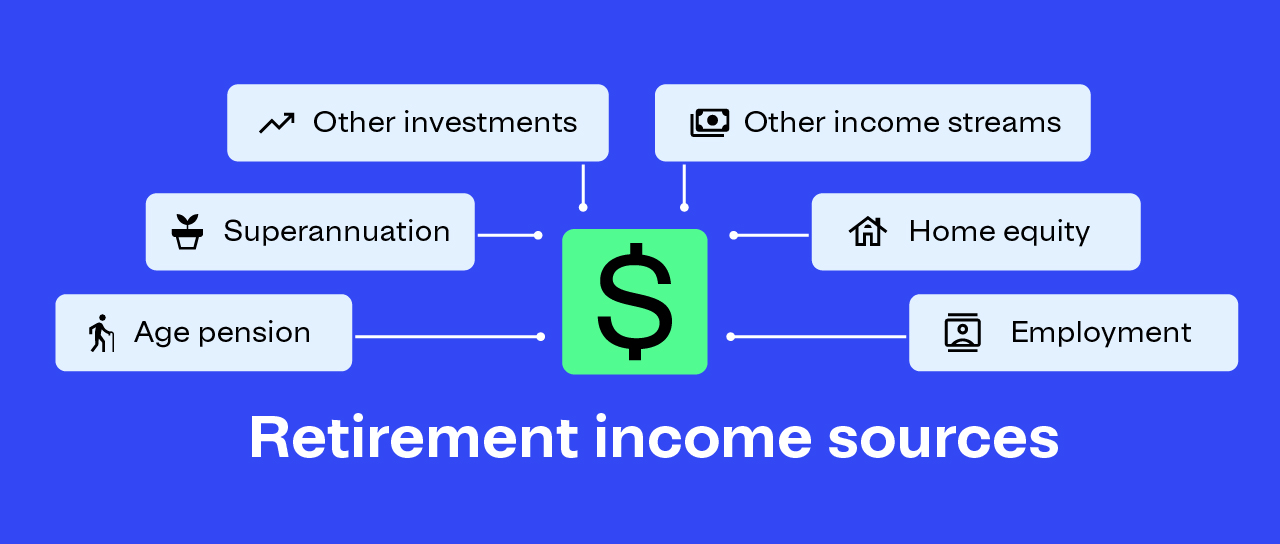

Age Pension and government benefits

For more than half of Australians, the government Age Pension is the foundation of retirement income. It provides a regular income to help with essential living costs.

Learn about Age Pension eligibility and benefits, and how to apply.

Michelle gets help to understand her income options

Michelle has worked in low-paid jobs for most of her life and has a low super balance. She owns her home but has little money saved. A few months before she turns 67, she contacts Services Australia’s Financial Information Service to understand her options. The service explains what documents she needs and how to apply. Michelle meets the income and assets tests, so Services Australia grants her the full Age Pension. With the Age Pension and concession card discounts, she can cover her expenses and live independently.

Superannuation income streams

For many Australians, super is the largest source of retirement income.

If you've reached preservation age (the minimum age the government needs you to be to access your super), you may be able to access your super in different ways.

You might do this while you're still working or after you retire. Options include:

- Transition to retirement income stream: a regular income funded by your super while you keep working.

- Account-based pension: a regular income funded by your super.

- Lump sum: you can choose to take some, or all, of your super at any time.

Transition to retirement income stream

A transition to retirement (TTR) income stream lets you take regular payments from your super while you keep working.

You can use a TTR income stream to:

- top up your income if you reduce your work hours

- boost your super and save on tax while you keep working full-time.

Before you start, check the rules for when you can begin and how much you can withdraw - minimum and maximum drawdown rules apply. Also check how it may affect your insurance in super or any government benefits you receive.

When you turn 65, a TTR automatically converts to an account-based pension.

Read more about transition to retirement.

Account-based pension

An account-based pension is a regular income stream funded by your super. You can choose:

- how much you want to transfer from super into the account-based pension

- the size and frequency of payments (as long as you meet the minimum drawdown rules)

- how you want the funds in your pension account invested.

Turning your super savings into a regular income stream gives you control over how and when you get paid. Read more about account-based pensions.

Taking a lump sum out of super

You might choose to take some, or all, of your super savings as a lump sum. If so, it’s important to keep in mind that your savings might be needed to support your retirement for many years. And check if taking money out could affect any insurance you have through your super.

Once you take a lump sum out of your super account, it's no longer part of the super system and you may not be able to put it back. If you invest the money, earnings on those investments are not taxed in the same way as they would be in the super environment. You may need to declare these earnings in your tax return.

Read more about taking super as a lump sum.

High-pressure sales tactics are putting your super savings at risk. Be on red alert for phone calls, click bait advertising and promises of unrealistic returns to encourage you to put your super into risky investments. Stop, think carefully, and check the claims first.

Read the investor alert and our tips on how to protect your money.

Other income streams

Annuities

An annuity pays you a guaranteed income for a set number of years, or for life. It can give you more certainty if other income changes. But annuities can limit when and how you can access your money.

You can use super, savings, or both to buy an annuity from a life insurance company or friendly society.

Read more about annuities in retirement.

Barry invests in an annuity

Barry has added to his super for years and has a healthy balance. He wants a steady reliable income that doesn’t rely on investment markets. After speaking with his financial adviser, Barry uses part of his super to buy a lifetime annuity. The annuity pays him a regular income for life. It also gives him confidence he can cover his needs, even if markets fall.

Lifetime income streams

A lifetime income stream pays you regular income for as long as you live.

You buy one with a lump sum, such as super or personal savings. The provider guarantees regular payments for life. This can give you more certainty about how long your income will last.

This product may be called a lifetime pension when you buy it from a super fund and a lifetime annuity when you buy it from a life insurance company or friendly society.

Buying a lifetime income stream with your super might increase your Age Pension, as special rules apply under the Age Pension income and assets tests.

Learn more about lifetime income streams. You can talk to your financial adviser about whether one suits you.

Working in retirement

Many Australians keep working for a while after they retire. Others return to work later.

The choice is yours. Even part-time or casual work can help pay expenses and draw less from your super.

If you plan to reduce your hours, you may be able to use your super to top up your income. See transition to retirement above.

If you get the Age Pension, Work Bonus lets you earn $300 per fortnight from work before it affects your pension.

Reverse mortgage and home equity release

If you own your own home, you may be able to use its value to help provide an income in retirement. Reverse mortgages and home equity release schemes let you access money from your home without selling it.

While these schemes can boost your income, they are not risk-free and it’s important to understand how they work and the long-term financial impact.

Learn more to decide if home equity release is right for you.

You could also consider downsizing your home to free up more money for retirement.

Other investments

Some people use income from other investments to supplement their retirement income. This may include interest from cash and term deposits, dividends from shares, or income from managed funds and other investments.

Interest, dividends and distributions can change over time, so what you get paid can change too.

How to Make Your Super Last in Retirement